4 Financial Reports Vital for Nonprofit Accounting

Very few people enter the nonprofit sector to put together financial reports. Those working at nonprofits likely started doing so because they want to make a difference in their communities. However, nonprofit accounting is essential to effective operations at the organization.

Just like

for-profits, how nonprofit organizations manage their finances will dictate the organization’s operational success. Their financial habits, like accurately reporting on their earnings and expenses, are a crucial part of attaining that success.

Nonprofits, however, develop a slightly different set of financial reports and statements than for-profit organizations do. This is because the goals are entirely different. While for-profits are working to earn money that can be taken home as profit, nonprofits reinvest all of their revenue back into the organization to promote growth and pursue their mission.

In this guide, we’ll walk through the four primary financial reports that nonprofits compile on a regular basis, what the reports are for, and the conclusions that can be drawn from them. We’ll cover the following:

- Statement of Activities

- Statement of Financial Position

- Statement of Cash Flows

- Statement of Functional Expenses

Of course, this isn’t the only vital element in

accounting for nonprofits, but it allows accounting teams to make financial decisions that will lead the organization to future growth. Let’s dive in.

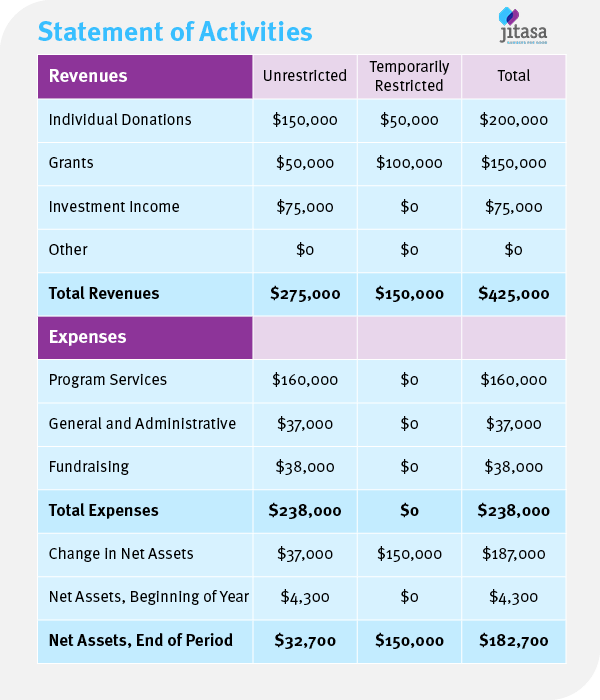

1. Statement of Activities

The first statement compiled by your nonprofit accounting team is the statement of activities. The for-profit version of this statement would be the nonprofit income statement. Essentially, this document is used to categorize the various types of revenue and expenses at the organization.

Nonprofits’ statement of activities will look different from the for-profit income statement because nonprofits often encounter restrictions associated with the revenue they receive. For example, let’s say

your nonprofit grant writing team writes proposals for several different grants that all have various restrictions associated. One can only be used for your scholarship program while another must be used for another specific program.

If you didn’t separate these out by restriction, it could be confusing to know how much funding you

actually

have to use freely on other initiatives. In the example below, you can see how different columns show the different restrictions placed on revenue.

The statement of activities also lists out your expenses, breaking them down into general categories. However, this isn’t a total breakdown of expense details. We’ll see that later in the statement of functional expenses.

Below the expenses, you’ll find the organization’s net assets. In this section, you’ll see that you can compare the net assets based on unrestricted assets, those with restrictions, and the total. Without this statement, nonprofits are at a risk of using the “total” assets and assuming it refers to the usable revenue at the organization. In reality, it’s less due to restrictions.

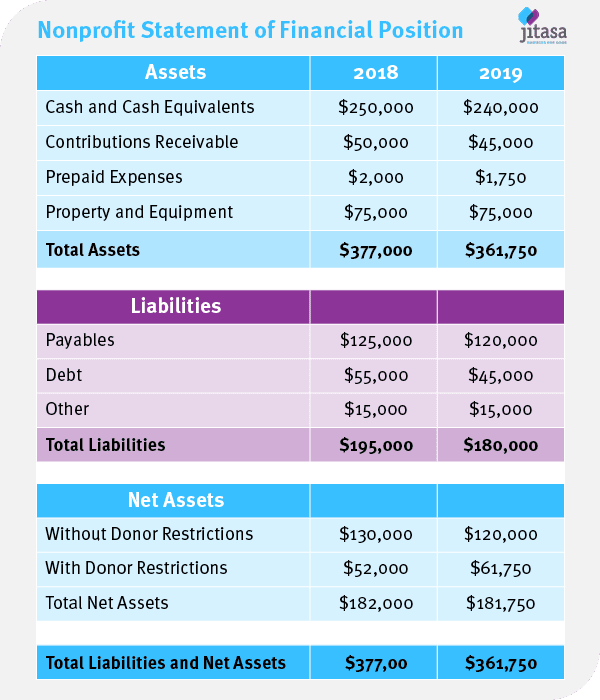

2. Statement of Financial Position

Similar to the statement of activities, your nonprofit’s statement of financial position also has a for-profit counterpart— the balance sheet. This statement is designed to provide a snapshot of the organization’s health at any particular point in time.

Your nonprofit’s statement of financial position breaks down your finances into the following sections:

- Assets. This section shows what your organization owns like cash assets, accounts receivable, prepaid expenses, and more. They’re listed by the amount of time it would take to make the assets liquid.

- Liabilities. This section shows what your organization owes including your accounts payable, debt, and other expenses. Generally you’ll have listings for your current liabilities (those owed within the year) and long-term liabilities (those paid over multiple years).

- Net Assets. Your net assets are simply your assets minus your liabilities. In this statement, they’re also listed out by restriction.

The following example was taken from

Jitasa’s statement of financial position guide, showing what this form might look like for an average nonprofit organization.

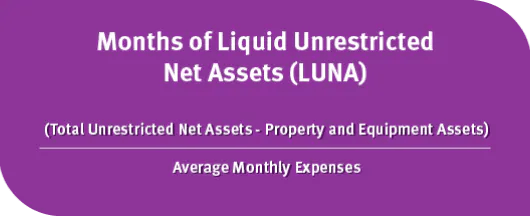

The purpose of this report is to show how much risk an organization can take on. Accountants may use the numbers in this statement to calculate your months of liquid unrestricted net assets (LUNA) using the following equation:

On average, three months of LUNA is a good place for nonprofits to maintain. If it dips below zero, they’ll need to immediately adjust their finances. Meanwhile, if it increases to more than three, the organization has the flexibility to take on additional risk at the organization, such as investing in new growth initiatives.

Consider how you can grow and expand while maintaining a

high engagement rate among your supporters. Over time, this will lead to more funding, additional flexibility, and a greater capacity to work toward your mission.

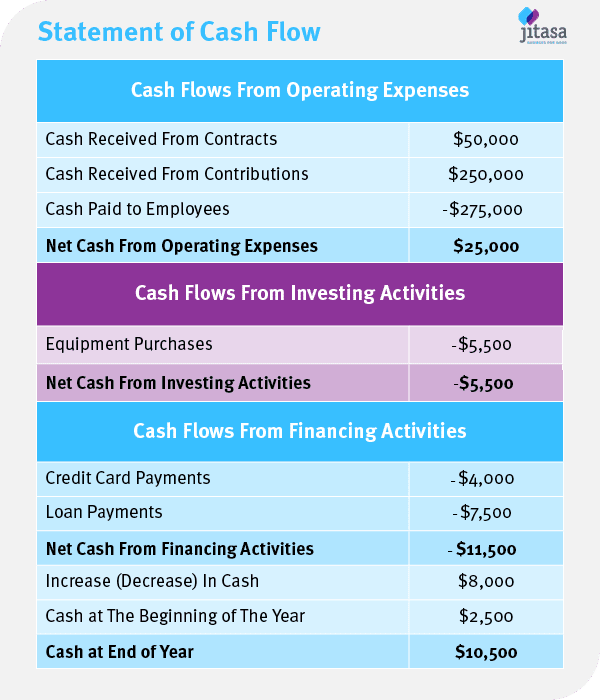

3. Statement of Cash Flows

Have you ever found yourself in the position of going out shopping, then realizing you need to check your bank account to be sure your next purchase doesn’t cause you to overdraft? Many individuals have encountered this stress. It’s not the type of stress that you want your nonprofit to encounter. That’s why organizations develop nonprofit cash flow statements. This report shows how cash moves in and out of your organization.

This statement breaks down your cash flow into your operating activities, investing activities, and financing activities. When you track the cash flow over time, you can gain new insights into the spending habits of your organization, helping to create more accurate budgets over time.

Your statement of cash flows will likely end up looking something like this:

If your organization carries any debt, your statement of cash flows can be incredibly helpful in finding out how much cash you have on hand to pay it down. Plus, as we mentioned, it can help you create better budgets in the future. If you know that the majority of your cash received from contributions comes from your year-end fundraising campaign, you can plan to spread out that cash throughout the following year in your budget, slowing down your cash flow.

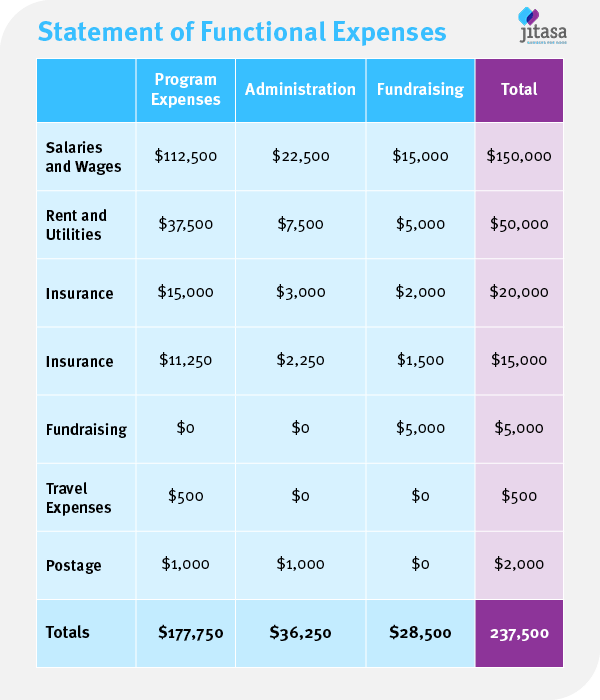

4. Statement of Functional Expenses

Your nonprofit’s statement of functional expenses describes the costs incurred for different areas of the organization. You probably spend the majority of your funding on the various programs and services that your organization provides to the community. But you also need to spend some funding on management and overhead expenses, as well as your fundraising costs. Those are the three main categories that are included on your organization’s statement of functional expenses.

When you compile your statement of functional expenses, it will end up looking something like this:

Individual donors ended up contributing $309 billion in the last year. Almost every one of those donors wants that $309 billion to be used solely for the expenses incurred doing mission-related work at the organizations. However, that’s not the reality of it.

Overhead expenses aren’t inherently bad! That’s why your functional expenses also include management and fundraising categories. It’s from here that you pay your staff, provide office space, and pay your bills. These are all necessary expenses to run your operations and to grow your organization. It’s necessary to strike a balance between your overhead expenses and those for program expenses. In general, try to keep at least 65% of your funding going towards your programs, but you can also recognize the necessity to increase some overhead to achieve growth.

Donors are starting to recognize that overhead expenses are essential for nonprofit growth. And, they can easily find the same information listed in the statement of functional expenses in your

annual tax forms. In fact, your Form 990 also requires your organization to categorize your expenses by general/management, fundraising, and programs. That means that your statement of functional expenses will only make it easier to file this form each year!

Financial reports are vital to understanding nonprofit funding. The information in these four reports can help your organization determine if it’s the right time for your team to expand, to reassess your financial situation, to start a new program, or to launch other growth initiatives.

About the Author

Jon Osterburg

Jon Osterburg has spent the last nine years helping more than 100 nonprofits around the world with their finances as a leader at Jitasa, an accounting firm that offers bookkeeping and accounting services to not for profit organizations.

SPEAK TO AN EXPERT

CONNECT WITH US

Join our newsletter for up-to-date Information